It continues to be debated, are we going to avoid a recession or have a soft landing? There has been concern about a recession for over a year. That said, it appears that the economy has been more resilient than expected in the face of restrictive monetary policy. Will this continue to be the case? Will this impact the American markets? This is where we will look together.

The current economic context

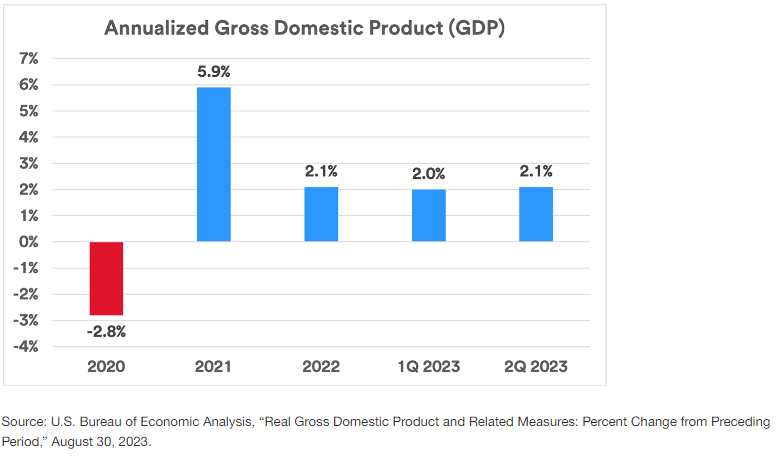

For now, we can say that despite the rise in rates, the economy has been resilient enough in the face of inflation and central bank policy to escape a recession. We can give credit mainly to a strong job market and a low unemployment rate. During the first half of the year, GDP was around 2%, which remains the long-term average. The 2% level is considered stable growth since it is average growth.

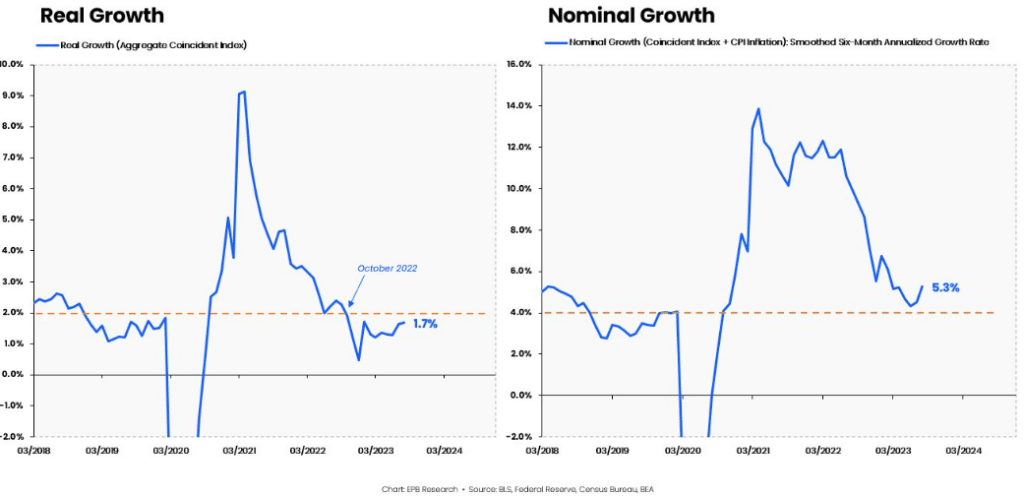

If we take into account the coincident figures which highlight employment, production, consumption and income. We find ourselves slightly below average in terms of real growth, and above average if we add inflation (nominal growth).

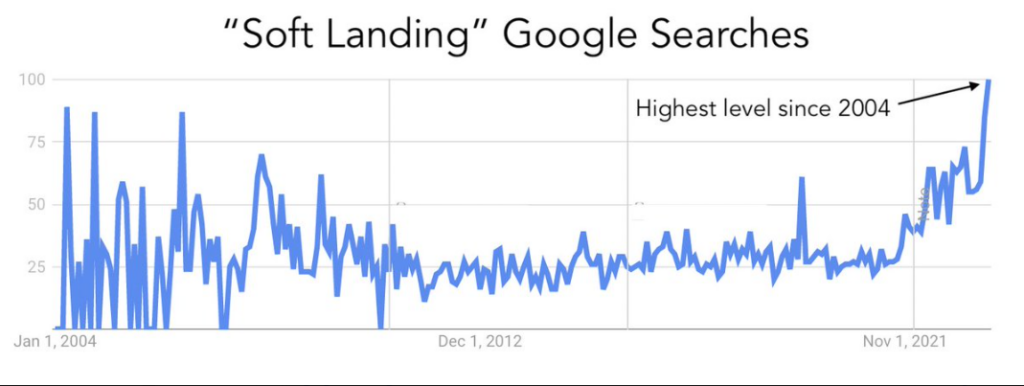

As much during the year 2022, there was a strong conviction of having a hard landing or a recession but this time, this trend has been reversed. Just like in 2008, operators were quite optimistic for a soft landing. However, this does not guarantee the outcome as can be seen in the graph below.

The job market helped avoid a recession

As explained previously, the job market has been a major factor in combating inflation. Since the Covid crisis, we have faced certain imbalances, particularly such as the labor shortage. For example, liquidity injections and the fall in rates have made it possible to generate quite a bit of performance at the asset level (real estate, ETFs, shares, etc.). These injections made it possible to get the US out of the recession caused by Covid. Some baby boomers did not return to work after COVID. Added to this is the strong one-off demand following liquidity injections. As there was more money in circulation, this generated greater demand for the same good, which translated into more labor needed.

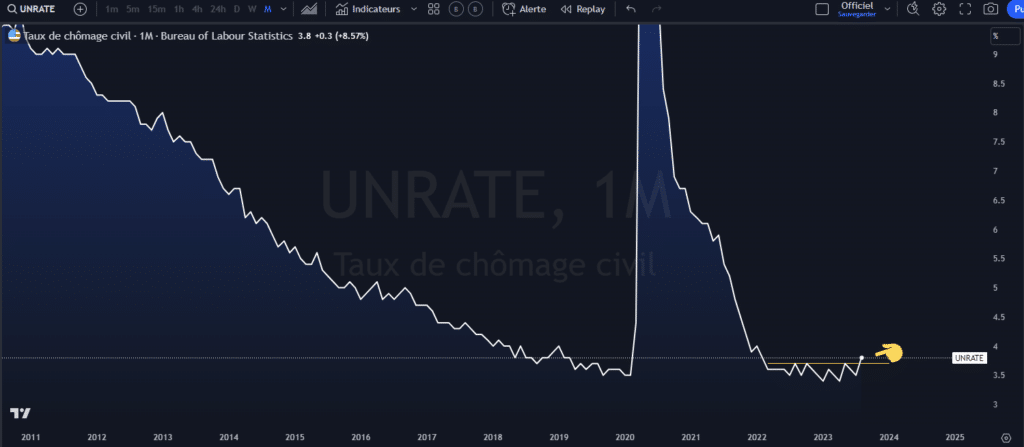

However, we can see the beginnings of fragility in the job market. Unemployment has just reached a new high.

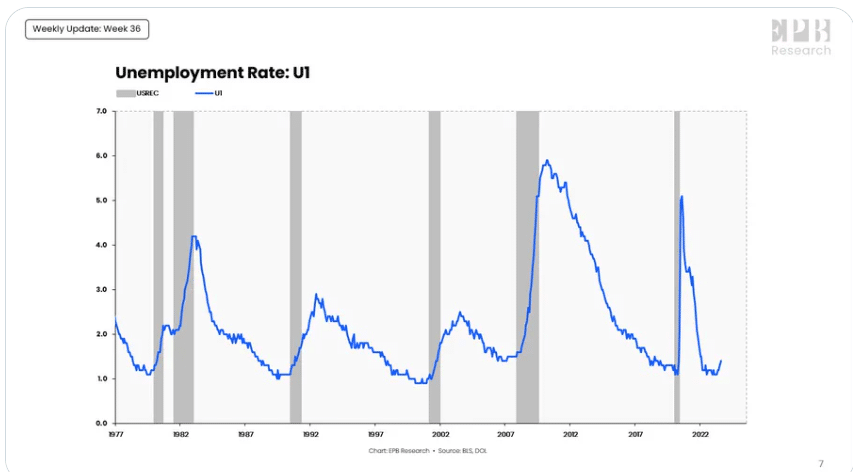

If we take the U1 indicator which represents the number of people unemployed for 2 weeks, we can also see a significant rebound.

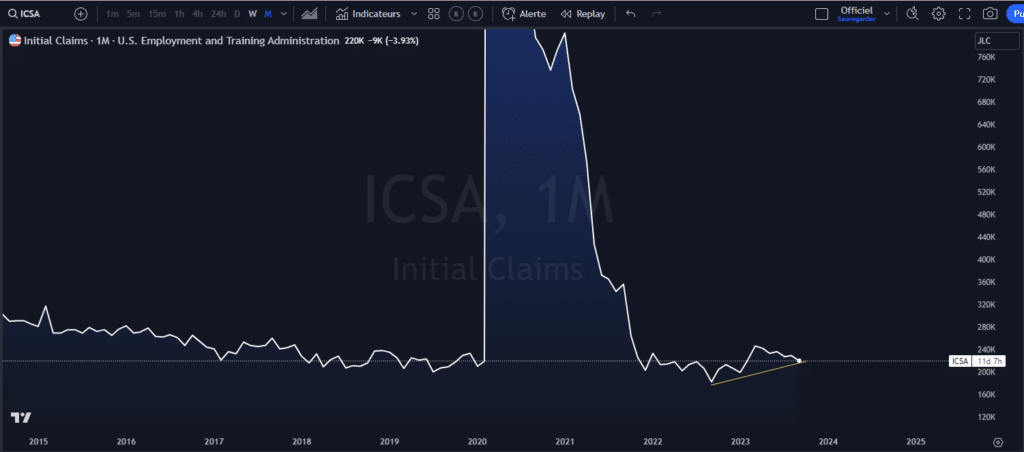

This is where you need to keep a close eye on initial claims. Before becoming unemployed, we must register to see if we are eligible for unemployment. This is a leading indicator. Therefore, it is supposed to give direction for unemployment.

If the job market was a major factor in maintaining a positive economy, we must still remain vigilant if this factor becomes increasingly fragile. For example, an increase above 4% could give some signals.

Rebounding inflation may increase recession risk

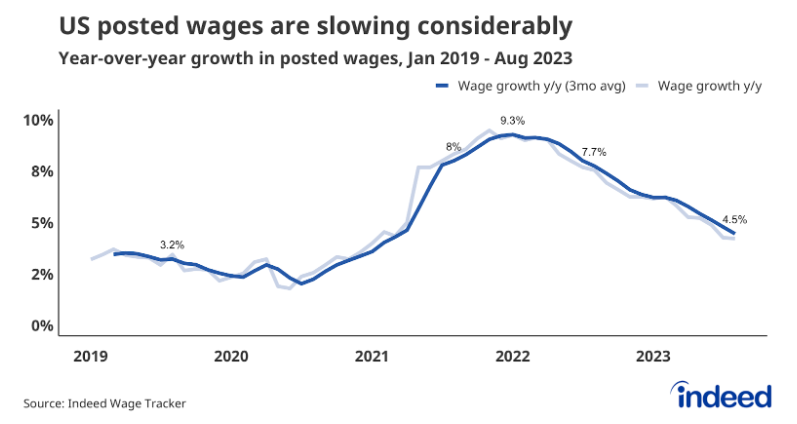

The last peak in inflation was in June 2022 at around 9%. Subsequently, inflation slowed in the following year via restrictive monetary policy. The rebound in inflation could once again be a problematic source. The rebound in raw materials as well as wage growth can maintain a certain level of inflation. Wage growth remains higher than inflation and production costs.

Therefore, this can generate inflation again. All this translates into a rebound in inflation in August which is likely to continue for September data since raw materials are still on the rise.

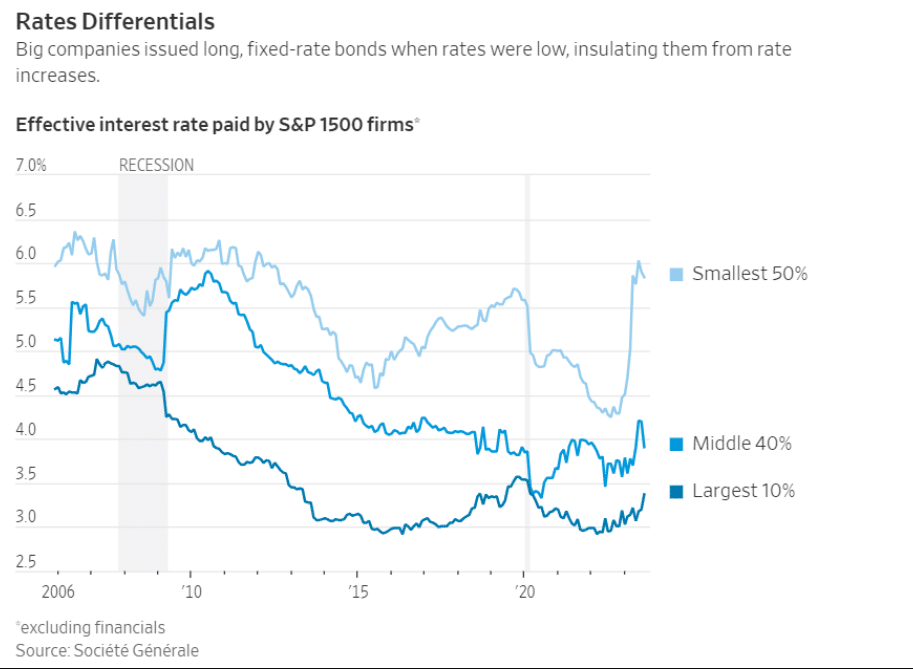

The other element to take into consideration is the CASH remuneration. Short-term rates are higher than inflation. For the richest, this remains a great risk-free opportunity to invest this money and make it grow. On the other hand, large caps issued long-term corporate bonds when rates were much lower. So, this allows them today to have positive rates between the borrowing rate (around 3.5%) and the cash remuneration rate of more than 5%. This can be considered stimulus, and can stimulate inflation.

This is where we could ultimately face stagflation which results in high inflation and increased unemployment. This kind of situation could make things difficult for central banks.

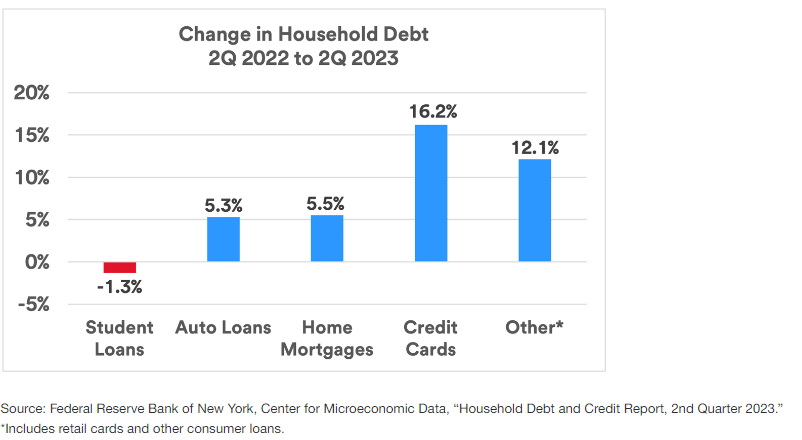

The level of consumer debt 2022 vs 2023

Today, we are in a different situation compared to 2022. We know that the job market was a major element in absorbing inflation. Thanks to this, they were able to maintain a certain standard of living and meet their needs.

From now on, we are in a completely different context. Rates have increased, and the level of debt has increased from 2022 to 2023. Particularly with regard to credit cards.

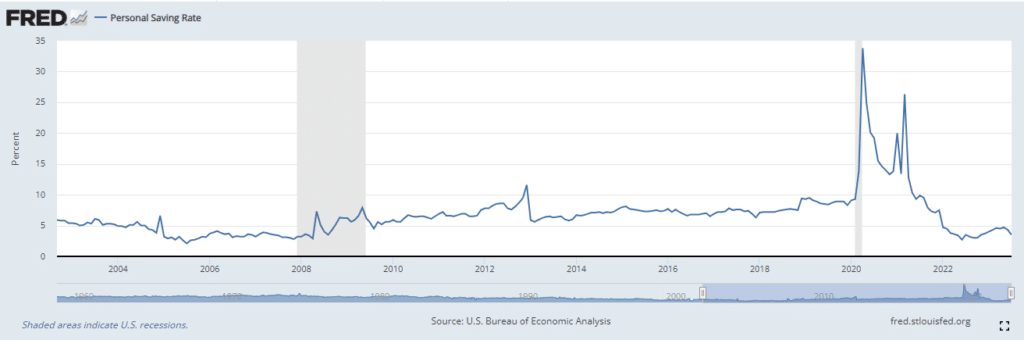

On the other hand, savings have declined sharply, which leaves fewer resources to meet loan repayment responsibilities and the job market is more fragile.

In 2022, the job market was turning with higher growth compared to growth of less than 1% today.

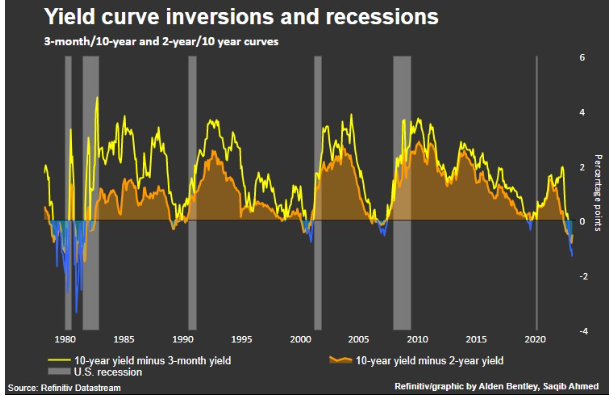

The consequences of an inversion of the curves

Generally, in the past, an inversion of the curves is often a signal of recession risk. This does not mean that we are in a recession, but it does mean that the risk of a recession is present. This is explained by the cycle of rate increases at the central bank level.

In the past, an inversion of the curves can give a signal 15 months in advance on average for the time between the inversion and the recession. This remains an average so the time can be less or more. In this case, the yield curve inversion took place in March 2022, so it’s been about 18 months.

The other element to also take into consideration is the consequences of a restrictive monetary policy. There is often a delay in the effects on the economy and this should not be underestimated. Therefore, we must remain vigilant, as we face the most aggressive rate hike cycle in history. A tomorrow without consequences in relation to this would be a first.

The impact on American markets

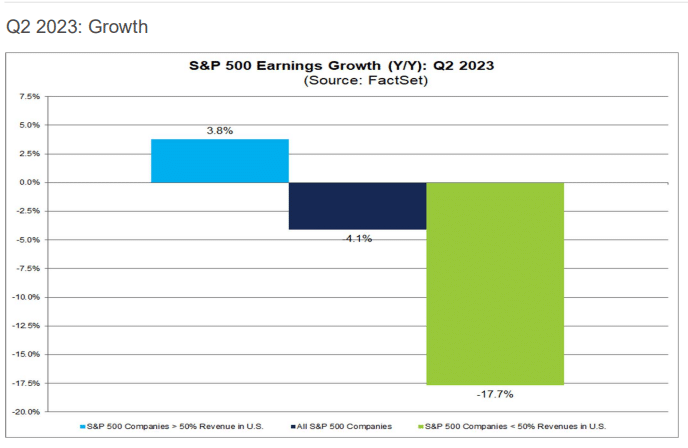

Even if the financial markets are not always correlated to the economy since it remains a market of supply and demand also in which investor sentiment plays a big role. That said, it very often ends up finding the balance between the two in the long term. Profits are the economy. Currently, we can see that profit growth remains weak since we are in an economic slowdown.

To justify current valuations, there would need to be either an economic rebound or a correction in valuations. For now, it will be difficult to have an economic rebound if inflation persists above the target rate forcing central banks to remain restrictive.

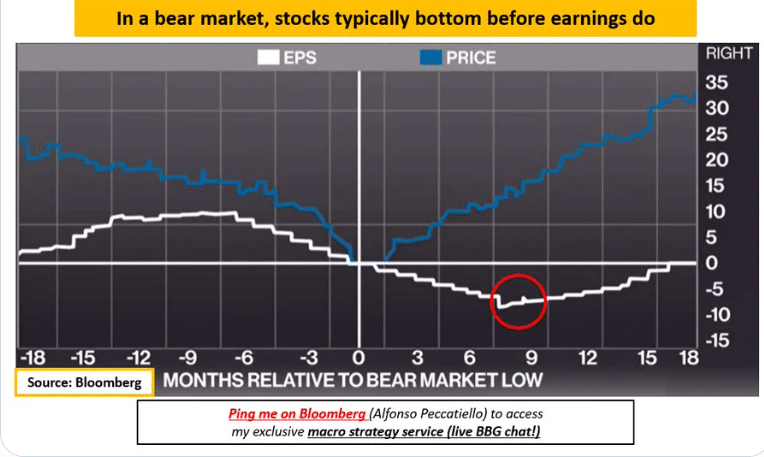

Statistically speaking, markets bottom 8 months before the lowest profits. Therefore, either we face a rebound in profits or there is a divergence that should be corrected.

Markets rarely bottom before a recession is pronounced by the NBER.

CONCLUSION

In 2022, job market growth and the level of savings were still high enough to cope with inflation. We are also still in the process of economic slowdown. A rebound in inflation could cause certain difficulties since it will be more difficult to absorb it compared to 2022. On the other hand, there is a significant expectation of a soft landing which remains similar to the 2008 context. It is precisely in this environment that we must remain vigilant. The central bank (FED) intends to remain restrictive as long as possible as long as inflation remains above 2%. Therefore, we cannot say that the American markets will avoid a recession as the risk remains present.

Receive a summary of the news in the world of cryptocurrencies by subscribing to our new service daily and weekly so you don’t miss anything of the Tremplin.io essentials!