State debt weighs heavily on the markets this week. Most assets find themselves heavily penalized by Fitch’s decision to downgrade its rating on US debt. Thus the agency points the finger at the high level of debt, the instability of the budgets, and the difficulties in finding agreements on the ceilings. The risk of public debt already weighed on the markets in May 2023, but now it seems to be generalizing to all the major over-indebted countries.

A degradation with serious consequences

At the end of May, the Fitch agency had already placed the American debt under “negative watch” because of the risk of default posed by the debt ceiling. Now, Fitch is realizing his concerns. Of course, the American debt remains for the agency among the best ratings, going from triple A (AAA) to double A (AA+). In our previous publication, we mentioned the more global risk on public debts (Public debt: A risk for the markets? – Tremplin.io).

“The US rating downgrade reflects the expected deterioration of public finances over the next three years, a high and growing general government debt burden. As well as the erosion of governance against ‘AA’ and ‘AAA’ rated peers over the past two decades, manifesting in repeated confrontations over the debt limit and last minute resolutions. »

The agency therefore invokes entirely fair and relevant reasons. Indeed, the United States has experienced in recent decades a growing laxity on its financial situation. Thus, the agency recalls that “The general government debt-to-GDP ratio is expected to increase over the forecast period, reaching 118.4% by 2025”. Moreover, “the debt ratio is more than two and a half times higher than the ‘AAA’ median of 39.3% of GDP and the ‘AA’ median of 44.7% of GDP”.

Despite everything, Fitch points out that if the United States can afford a higher level of indebtedness, it is because of the strength of the dollar. But the agency also foresees a recession for the American economy in the last quarter of 2023 and the first quarter of 2024. Growth in 2024 would only be +0.5%.

“Several structural forces underpin US ratings. These include its large, advanced, well-diversified and high-income economy, supported by a vibrant business environment. Above all, the US dollar is the world’s main reserve currency, giving the government extraordinary flexibility in funding. »

Finally, no reduction in the key rate is expected before at least March 2024. In this context, Fitch shows that the government should support a weak growth of its resources and an increase in its interest charge.

The dark scenario for the public budget

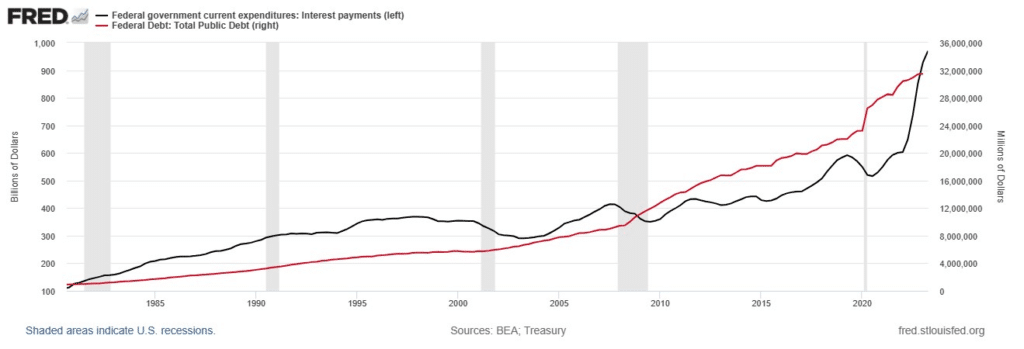

In the space of a single year, the federal government’s interest charge has increased by +35%! THE New York Times also recalls that the interest charge is expected to exceed the military budget in the coming years. The chart below shows the level of US debt (red line) and interest payments (black).

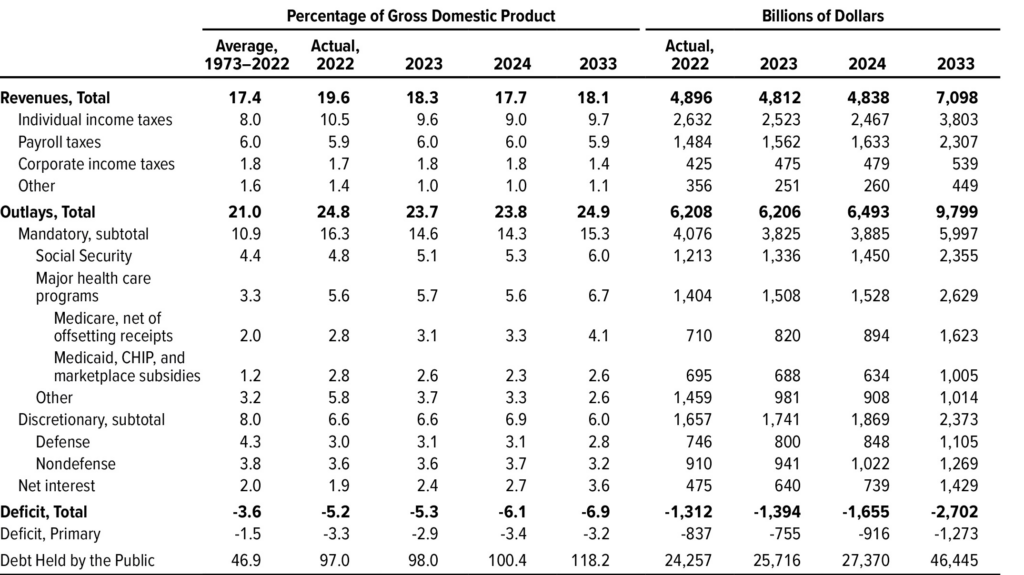

The anticipated budgets for the coming decade attest to a deterioration in the country’s financial satiation. Thus, Congress recalls that $640 billion should be used to repay the debt in 2023. The deficit, at more than 5% of GDP, should not be reduced so soon. By 2026 or 2027, the interest charge is likely to exceed the already considerable defense budget. The latter represents approximately $800 billion in 2023. In France, the first state budget between now and 2027 will be the interest charge, ahead of education. The table below presents the anticipation of the future situation on the federal budget.

Because in addition to the deterioration of finances, there are a certain number of structural factors. Fitch’s press release recalls the following elements. The funds dedicated to social protection would even be exhausted within 10 years. Consequently, this degradation appears to be more durable and more justified than any before.

“Over the next decade, higher interest rates and rising debt stock will increase the interest service burden, while the aging of the population and the increase in health costs will lead to higher spending on older people in the absence of fiscal policy reforms. The CBO predicts that interest costs will double by 2033, to 3.6% of GDP. The CBO also estimates an increase in mandatory spending for Medicare and Social Security of 1.5% of GDP over the same period. The CBO predicts that the Social Security fund will be depleted by 2033 and that the hospital health insurance fund (used to pay benefits under Medicare Part A) will be exhausted by 2035 under current laws, posing additional challenges to the fiscal trajectory unless timely corrective measures are implemented. »

The fall of the markets

The markets, despite the negative watch, were surprised. Bitcoin briefly hovered around $28,500 on August 1. For its part, the price of the yellow metal remained stable. An interesting reaction is also noticeable on the VIX, the volatility index of the S&P 500. The latter has climbed by +18% over the past week to return to the level of 16. A move of the VIX above 17 could trigger a more lasting wave of market stress.

The CAC 40 thus opened sharply lower and broke the attempted rebound initiated at the end of July. But the most strategic information comes to us from the reaction of the bond market. The rate on 10-year bonds for the United States is back above 4%. In a context where the key rate is 5.5%, and where budget projections may even seem optimistic, we are taking stock of the wave of difficulties to come between now and 2030.

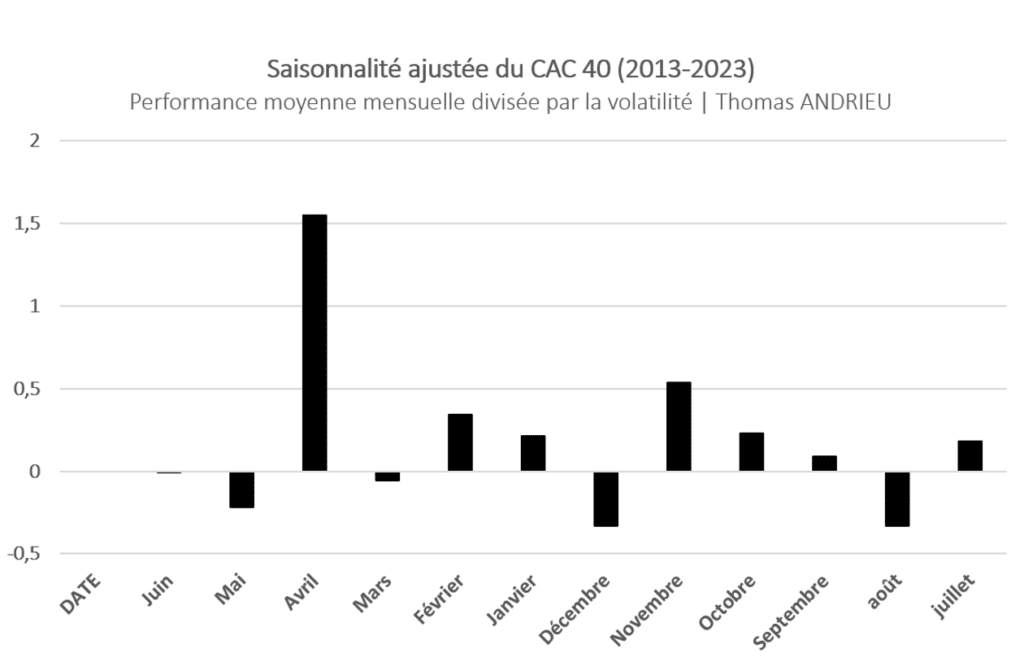

The seasonality at work of this degradation?

We know that the month of August is often synonymous with stagnation or decline for indices. This news therefore seems to correlate perfectly with the beginning of August. While the month of July generally shows a slight increase (the latter ended up +1.3% for the CAC 40), the month of August generally heralds a corrective wave. Of course, these are averages and statistical dispersions which cannot determine everything. But there are months more conducive to this type of announcement which is sometimes likely to change the psychology of the market.

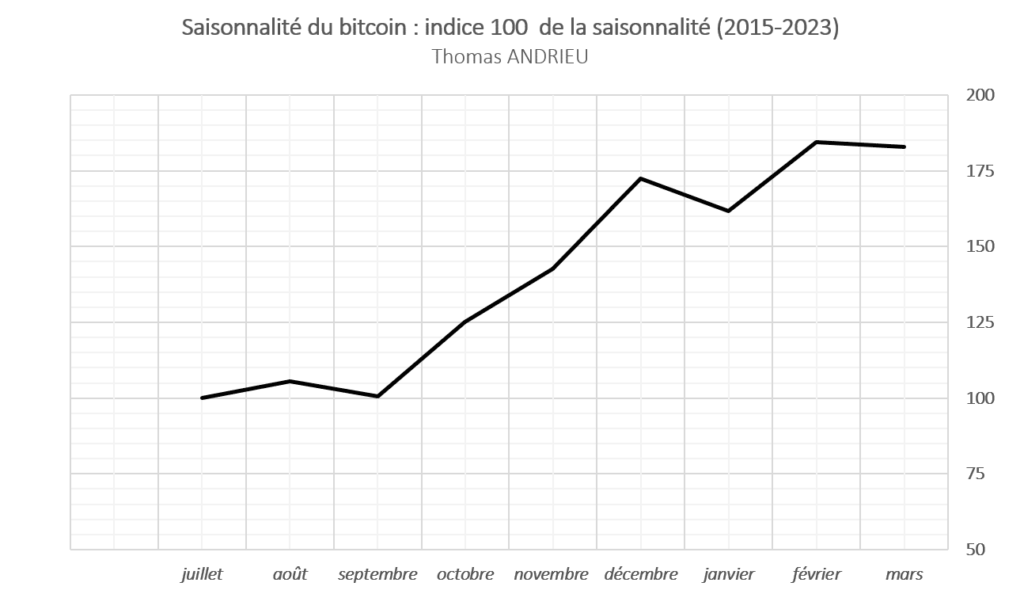

In addition, we have already had the opportunity to expose the seasonality of bitcoin (The seasonality of bitcoin (BTC) – Tremplin.io). While July generally shows some progress, August is more bleak. It is often the month of September that results in more persistent corrections.

Therefore, it seems important to us to specify that the deterioration of Fitch is perhaps likely to finalize the trend of the summer. However, given the scope of the analysis, this news would not be likely to cause a sharp correction in the markets.

In conclusion

Ultimately, the “negative watch” rating agency Fitch ultimately led to a downgrade. The long-term debt of the United States was thus downgraded from AAA to AA+. In question, the excessive level of debt, which remains 2.4 times higher than the median of indebtedness of this category. In addition, the budget forecasts show a growing deficit and a growing interest charge. Within 5 years, the interest charge could exceed the famous US Defense budget. The concern also relates to certain social security funds, which could be in deficit within 10 years. This deterioration is amply justified, and the risks weighing on the debt ceiling accentuate this analysis.

The American public debt is the most consistent of the developed countries, so it is clear that this event should not be underestimated. The impact on the financial markets was rapid and clearly negative. However, if this event also occurs with seasonality, it is not likely to significantly degrade the medium-term trend.

Receive a digest of news in the world of cryptocurrencies by subscribing to our new service of daily and weekly so you don’t miss any of the essential Tremplin.io!