Among the elements that explain the market correction in August, we find the rise in the bond rate. In this paper, we will focus on the role of the bond rate and its implications on financial markets. Furthermore, Jackson Hole and the decisions of central banks could considerably influence the evolution of financial markets in the coming months.

An inexorable rise in rates

The trend of rising bond rates has continued for 3 years now. In the summer of 2020, the 10-year US government rate was close to +0.6%. It now stands at more than 4.25%. This rate level simply corresponds to the highest level since 2007. But the records on long rates hide another aspect. Indeed, the Fed’s key rate is between 5.25% and 5.5%. That is to say that investors prefer to be paid 4.25% on a long bond than 5.25% on the interbank market.

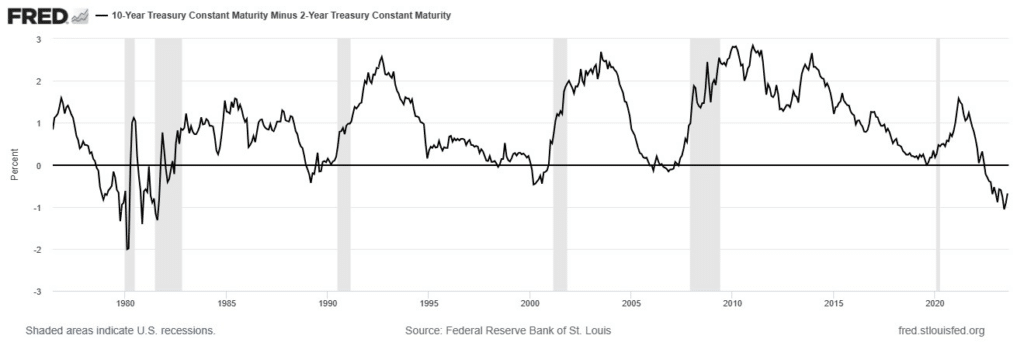

Obviously, investments include in their expectations a fall in inflation and various risks in the coming years. This explains why the long rate is up to 1 point lower than the short rate. Indeed, the rate of the treasury bill, the 3-month bonds of the American government, amounts to 5.3%. A long rate higher than the short rate, when it returns to normal (long rate > short rate), often heralds a recession. Consequently, the fall in the short rate, or the marked rise in the long rate, would be likely to herald an approaching recession.

But for the time being, the markets are undergoing a rate hike that is not yet complete. Moreover, the maintenance of underlying inflation and the deterioration of financial conditions are contributing to this rise in rates.

“ The long-term debt of the United States was thus downgraded from AAA to AA+. In question, the excessive level of debt, which remains 2.4 times higher than the median of indebtedness of this category. In addition, the budget forecasts show a growing deficit and a growing interest charge. Within 5 years, the interest charge could exceed the famous US Defense budget. The concern also relates to certain social security funds, which could be in deficit within 10 years. This deterioration is amply justified, and the risks weighing on the debt ceiling accentuate this analysis.“

The threatening deterioration of debts – Tremplin.io

Fall on the markets

Rising interest rates cause bond values to fall. Indeed, investors prefer to sell bonds with lower rates to buy bonds with higher rates. This is all the more impacting as the bond market is the leading market in terms of valuation ahead of equities. As a result, the rise in rates reduces, on the one hand, access to credit and investment (therefore growth prospects), and on the other hand, it reduces the attractiveness of stocks (for which dividends may then appear weak).

Under these conditions, all markets are impacted. Stocks, cryptocurrencies, and even gold, have undergone corrective movement. Cash is becoming scarcer, volumes lower, players more cautious. Rising long rates therefore limit the growth potential of indices and financial markets.

Conversely, a lasting bull market is only possible in the case of stagnation or a lasting decrease in long rates. But the stagnation of long rates will certainly correspond to a stagnation of the economy. Which worsens the prospects for a rebound.

An impact on currencies

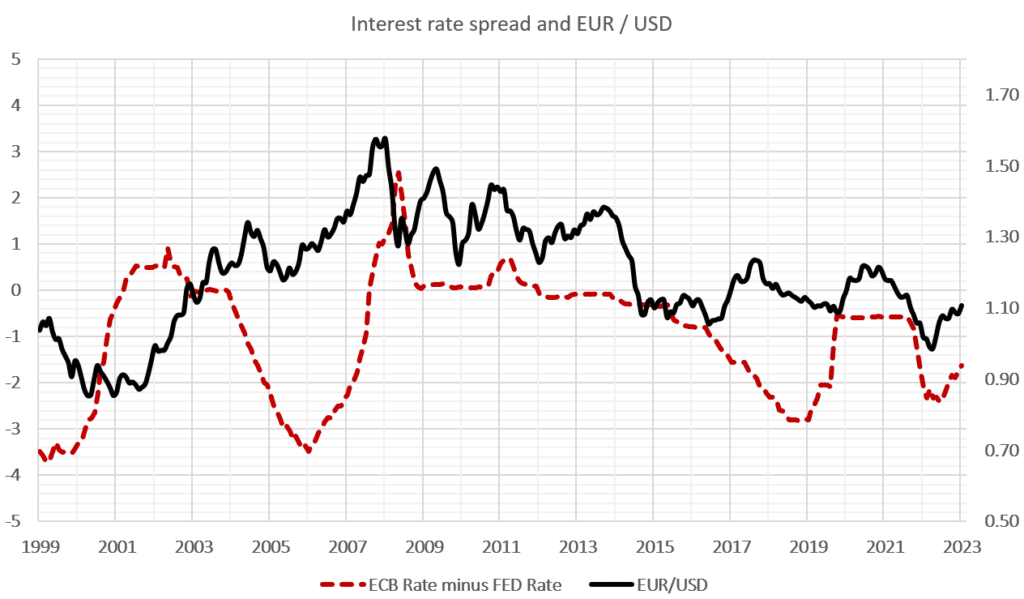

The currency market is also strongly impacted by these rate changes. In recent months, the dollar has been penalized by a more persistent bearish movement. Nevertheless, this movement is explained by the fact that the ECB is trying to catch up in the fight against inflation. But it is clear that the euro’s rebound is not structurally strong enough to be accelerated so far. The chart below shows the euro/dollar parity and the rate differential between the euro zone and the United States. A pivot from the FED, without a pivot from the ECB, would be likely to favor the price of the euro. However, the Jackson Hole meeting could relatively synchronize these rate pivot decisions.

Additionally, it is important to note the following. First, the Eurozone has stickier inflation. Then, the flexibility of the euro zone economy is quite low compared to that of the United States. Consequently, although the euro zone would require a stronger increase in key rates, the ECB ensures the health of public finances and businesses. The ECB is therefore probably acting in a way to limit the fall of the euro (imported inflation) and to fight against inflation in the wake of the FED.

A persistent financial risk

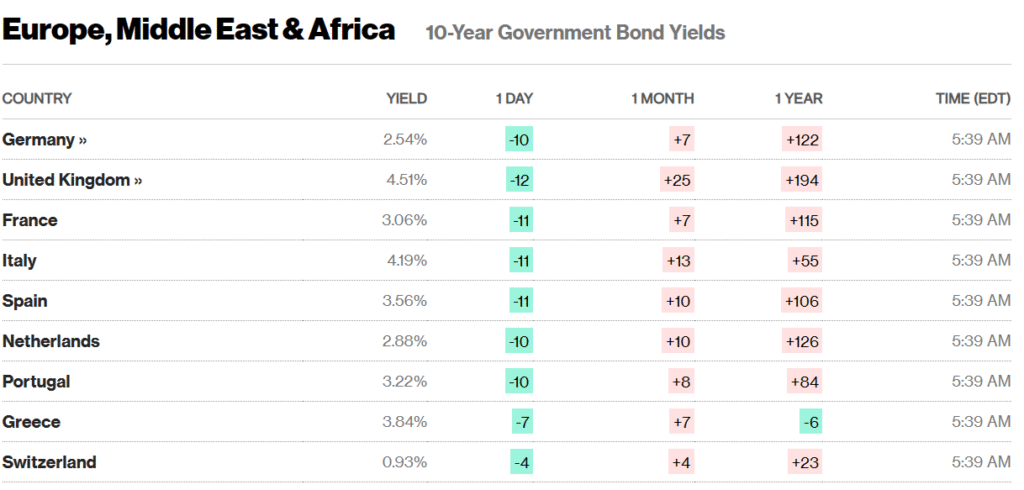

In the euro zone, sovereign rates are between 2.5% (for Germany) and 4.2% (for Italy). That’s a difference of 170 basis points. Over one year, the countries which experienced the largest rate increase were the United Kingdom, the Netherlands, Germany, France and Spain. Despite everything, certain European rates remain below the ECB’s key rate, which again indicates an inversion of the yield curve.

The economist Patrick Artus shows, assuming that the interest charge would represent 3.5% of French GDP in 2027, that public deficits will be very high. Indeed, “the total public deficit in 2027 would be: 4.7% of GDP in France; 3.7% of GDP in the euro zone ». Under these conditions, it is clear that each rate increase for governments and businesses would have a very negative impact in the future.

The rise in rates therefore weighs heavily in the long term, and it is likely that the rise in long-term rates will not be quickly reversed for a few years. Indeed, the high level of debt in many countries, and the high level of interest charges, suggests persistent financial deterioration.

Jackson Hole in the viewfinder

The term “Jackson Hole” refers to the annual meeting hosted by the Federal Reserve Bank of Kansas City. This event, officially known as the Federal Reserve Bank of Kansas City Economic Policy Symposium, is taking place in Jackson Hole, a city located in the state of Wyoming in the United States.

The Jackson Hole meeting brings together central bank officials, economists, academics, heads of financial institutions and other experts from around the world to discuss current and future economic and monetary issues. The event usually takes place at the end of August and lasts over several days. It is truly a question of setting the global monetary tempo.

Maintaining the job market and underlying inflation are at the heart of discussions this season. Central banks therefore always seek to fight inflation, but any deterioration in the job market, or a sufficient reduction in inflation figures, would be likely to lead to an end to the increase in key rates. With this in mind, economists also strive to define the neutral rate for the economy. That is to say the rate which allows the economy to function without generating too much inflation.

In any case, it seems very unlikely that the period of low rates will return. Therefore, investors must incorporate a certain number of risks which did not exist until now (inflationary risk, interest rate risk, default risk, deterioration of finances, etc.).

In conclusion

Ultimately, we have seen that bond rates are pushed to new heights, still three years after the start of this increase. This trend, which seems endless to some, still weighs on the markets. In addition, if central banks are still partially or completely continuing to raise rates, the gap between short rates and long rates remains high. An increase in long-term rates would therefore above all reflect a reduction in the gap with short-term rates. This may also reflect the fact that investors have a more negative outlook on long-term inflation. But at the same time, the reduction in the gap between rates would soon herald a recession, which would also favor the stagnation or fall of key rates.

The meeting in Jackson Hole reaffirms the objectives of central banks to fight inflation, and the attention of economists is primarily on the job market. In any case, the rise in rates breaks 10 years of quantitative easing. As long as long-term rates remain under pressure, it is likely that the financial conditions will not be in place for upward dynamics.

Receive a digest of news in the world of cryptocurrencies by subscribing to our new service of daily and weekly so you don’t miss any of the essential Tremplin.io!