The last peak of inflation was reached in June 2022. For more than a year, we have had a gradual decline in inflation supported by the implementation of a restrictive monetary policy. From now on, we face a risk of a rebound in inflation at the end of the year. Have we bottomed out on inflation? What are the implications for bitcoin and financial assets in general? Are we going to enter a stagflation phase? This is where we’re going to look at all of these points together.

Waves of inflation

Before we begin, we will highlight the fact that inflation could return several times during this decade. Here are some reasons:

- The climate transition remains inflationary

- Deglobalization is inflationary

- One of the ways to reduce debt remains inflation

- Other liquidity injections to be expected during the decade because of the deficit

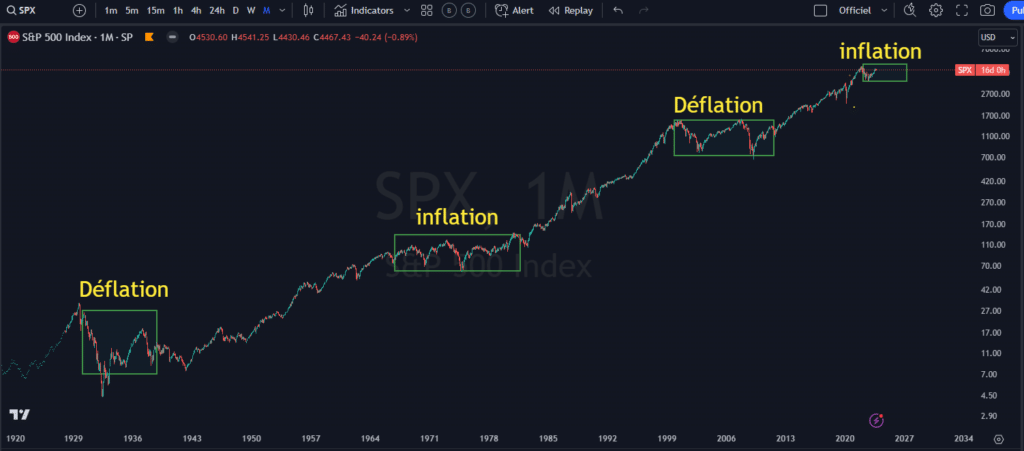

In the past, we have faced periods of inflation, disinflation and deflation. When we have a regime change, there can be a decade of adaptation. And as you can see, this can have an impact on the stock market. Here is the link between regime change and the variation in the S&P500:

The other important point is to look at how the inflation trend is well underway since the COVID crisis, a major catalyst. It is not the pandemic itself that is the cause but rather the consequences of the measures that were taken to overcome covid such as injecting liquidity, or stopping the supply chain for example.

Liquidity injections are inflationary

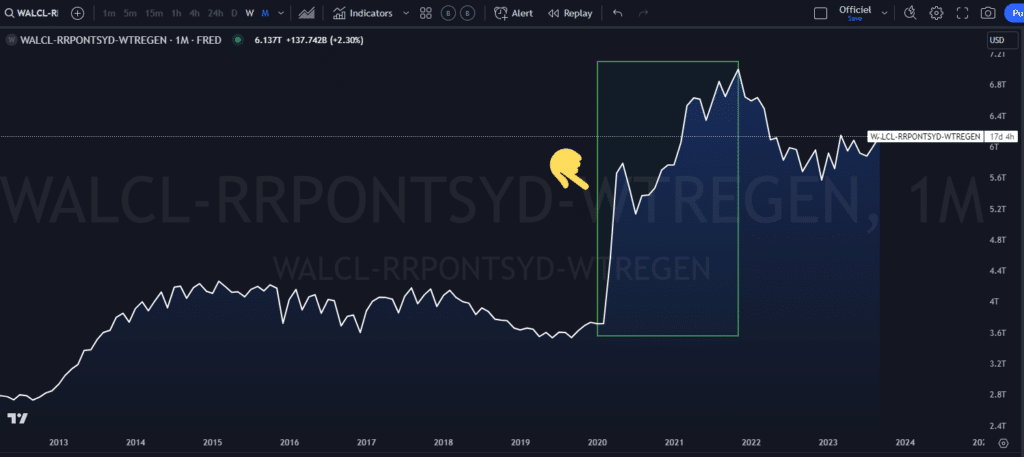

As we saw earlier, liquidity injections caused much of the inflation. Moreover, we can see the increase in the net liquidity of the FED during 2020:

The more we increase the money supply, the more this translates into more money in circulation. If at the same time, production remains the same (constant), this can create an imbalance because there is more money in circulation to buy the same good. As a result, the price of the good increases.

Bottom of inflation?

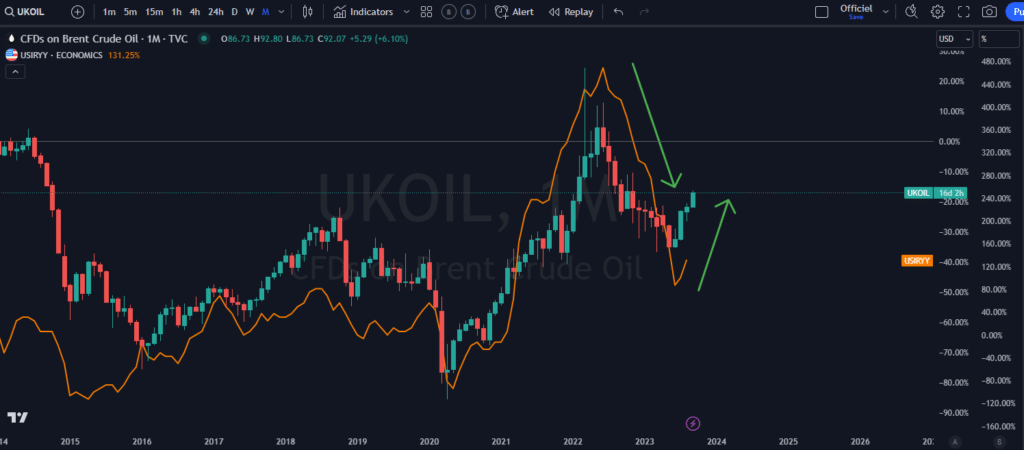

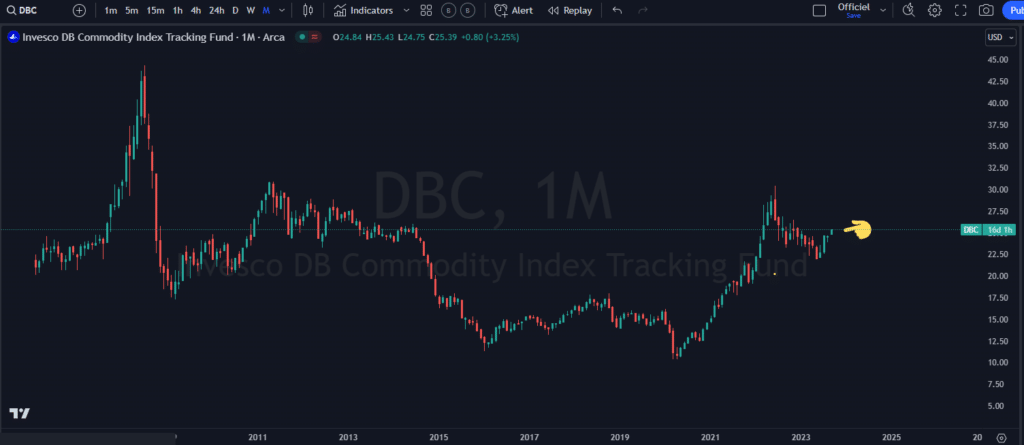

There is a likelihood of a bottom followed by a rebound in inflation. Even if monetary policy still had its effect in reducing inflation. It turns out that’s still not enough. We can see a certain rebound in commodities which may make the FED’s task in bringing down inflation more difficult. You can see in the chart below that the fall in oil has contributed significantly to the fall in inflation. It is the same in the other direction.

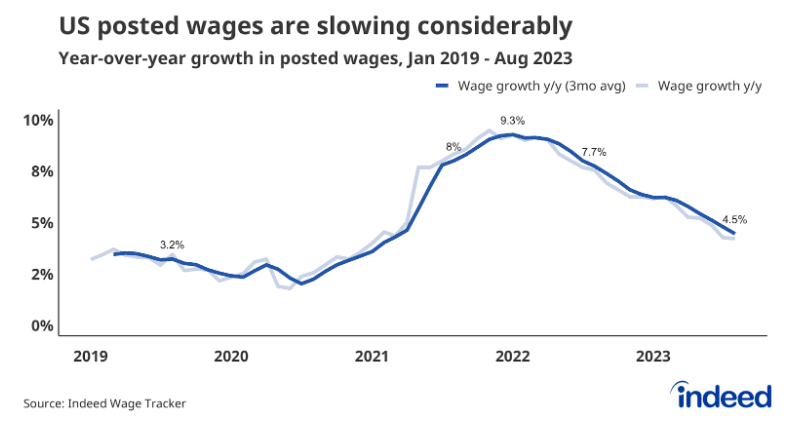

The other element which risks putting pressure on inflation remains wage growth. This is currently around 4-5%. This figure is both higher than the level of inflation and production costs. As a result, we may face a wage-inflation spiral. That is to say, wage growth can put further pressure on prices.

This risks making the FED’s task more difficult in the coming months even if they seem quite confident of a soft landing. The contradiction here is that it will probably have to affect the job market to bring inflation down to desired levels.

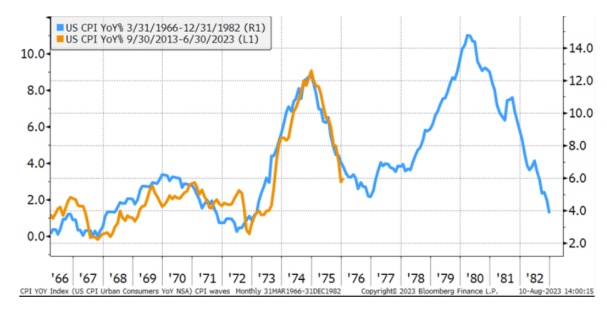

If we face a decade of inflation, there should be multiple waves of inflation that include multiple bottoms and rebounds. It could be that in this case, the bottom remains around 3%. Here’s a chart that compares today’s inflation with the inflationary waves of the 1970s.

A context of stagflation?

A stagflationary environment results in low growth and high inflation. Currently, we have a growth level close to 1% when we take the coincident figures (employment, consumption, production, income). And inflation remains quite resilient above 3%.

If inflation rebounds, this could cause complications, particularly in the job market since we could face a situation of stagflation. To confirm this type of context, we would also need an increase in unemployment. We can see a slight increase in unemployment since we went from 3.2% to 3.8%. A move above 4% could be much more significant.

Inflation via fiat currency

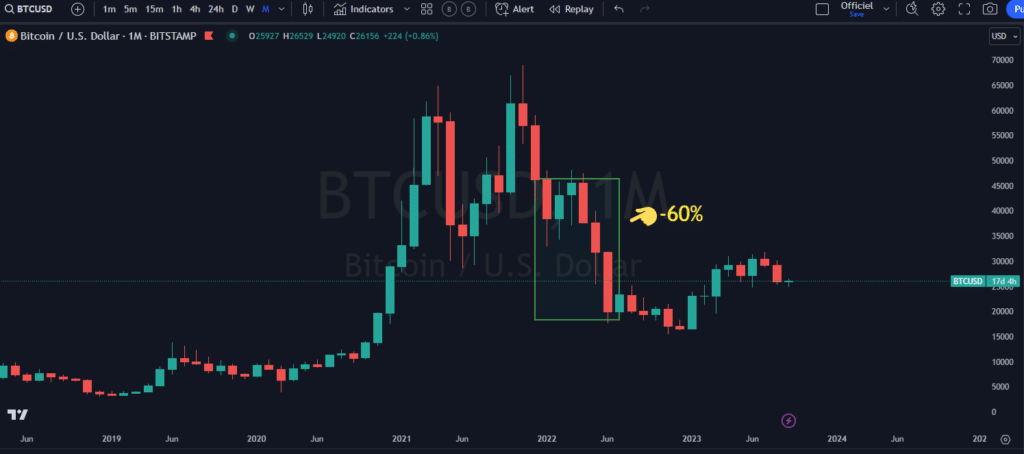

It has often been said that bitcoin would be a hedge against inflation. That said, it has not been an inflation hedge in 2022. A mix of economic slowdown, inflation and restrictive policy has not been a good cocktail for many assets. As a result, bitcoin fell by more than 50%. The good side of a bear market is that it frees companies from questioning their credibility.

Inflation can arise in different ways. In 2022, it is the consequences of recovery programs, in particular liquidity injections, which have largely caused inflation. As soon as we increase the money supply, we can have inflation via fiat currency (local currency) since it is an increase in the monetary supply. We will take the example of inflation and deflation via fiat currency:

- Inflation via fiat currency = expansion of monetary supply

- Deflation via fiat currency = decrease in monetary supply

Bitcoin is not a fiat currency since it is a cryptocurrency. It has a limited supply since it is designed to mine 21 million bitcoins. On the other hand, the principle of halving allows the supply to be gradually reduced every 4 years until the total number of bitcoins is mined. Bitcoin remains an offensive against the expansion of the monetary supply of fiat currency, provided that the supply remains constant.

The impacts of inflation on bitcoin

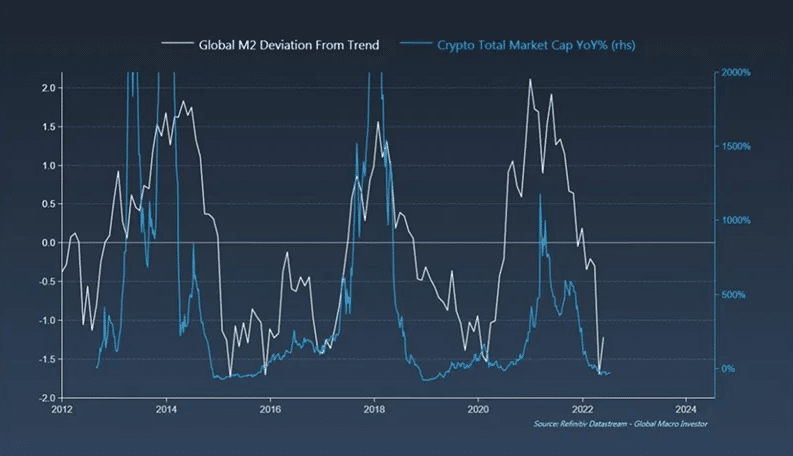

When we are in a period of inflation, central banks will seek to reduce the monetary supply using different tools. Therefore, this makes financial conditions more restrictive. As bitcoin remains an asset that outperforms during periods when financial conditions are more accommodative, this could make the task more difficult. Periods where financial conditions are quite accommodative is often when we have an expansion in money supply. We can see in the graph below the link between the monetary supply and bitcoin. For example, when it increases, it is favorable for bitcoin and vice versa:

Inflation is not a bad thing when the economy can absorb it well. For example, if we are experiencing accelerating growth, it is easier to absorb inflation.

If we have a rebound in inflation, it would rather come from a rebound in raw materials (decrease in supply) and wage growth. For example, wage growth is around 4-5%, which remains higher than both inflation and production costs. Therefore, this kind of situation can boost new prices. On the other hand, we must monitor the rebound in raw materials.

When consumer prices rise, it involves several things. First, consumers will have less disposable income. So, they will prioritize spending on basic needs like food or gasoline. This also means that there will be less liquidity left for secondary needs or to invest in bitcoin or other things. This kind of situation could keep bitcoin in the 20-30k range, limiting the upside potential.

CONCLUSION

A rebound in inflation could limit the performance of bitcoin since consumers will have less income available to invest in bitcoin. And as we are still in the process of economic slowdown, it will be difficult to absorb a further increase in inflation. It is important to add that bitcoin is rather an asset that appreciates an environment of disinflation and deflation.

Receive a summary of the news in the world of cryptocurrencies by subscribing to our new service daily and weekly so you don’t miss anything of the Tremplin.io essentials!