USDT de Tether and USDC de Circle has long occupied the summit of the Stablecoins sector. For years, these two workers constituted almost the entire market, leaving little room for others. This landscape is now changing. Their combined share decreases in the face of new competitors, regulatory executives and banks that are starting to reshape the sector.

In short

- USDT and USDC saw their market share drop from 91% in March 2024 to 83% currently, signaling the growing influence of rival stablecoins.

- These new Stablecoins attract interest by offering investors, providing viable alternatives to traditional leaders.

- Large banks also explore their entry into the Stablecoins market via potential consortia, a movement that could deeply reshape the sector.

Decrease in the dominance of USDT and USDC

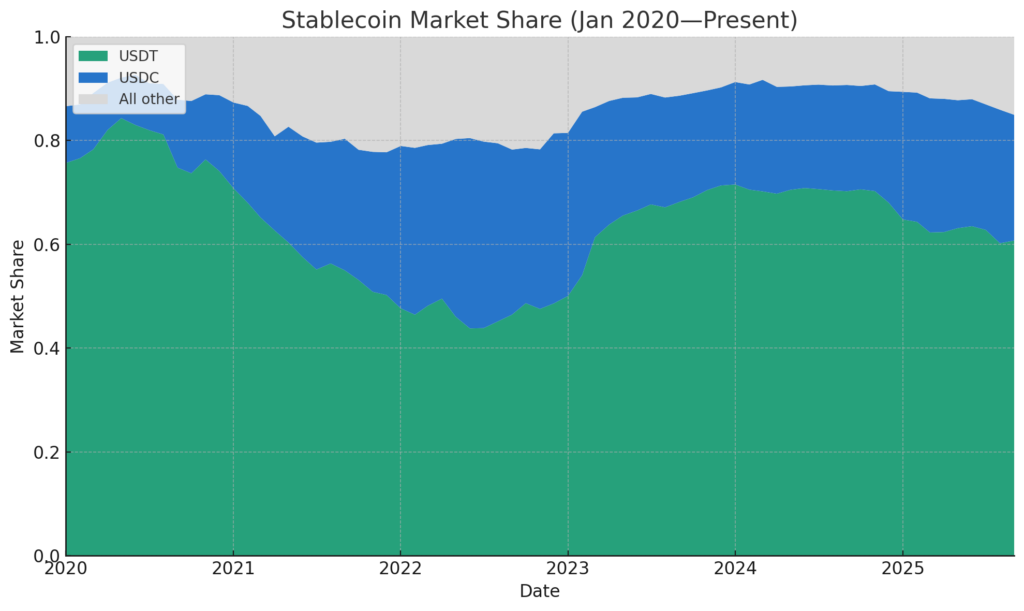

The global Stablecoins market was estimated at more than $ 140 billion, with USDT around 103 billion and USDC at around 29 billion in March 2024, representing together 91.6 % of the total supply and giving the two parts almost a complete market control.

This dominance began to decrease. Defillama's data show that USDT and USDC now represent 83.27 % of the Stablecoins market sharea drop of more than eight percentage points, signaling a slow but regular erosion of their control. Analyst Nic Carter stresses that this downward trend should continue, stimulated by increasing structural and competitive pressures on the market.

New stablecoins compete in yield

Carter underlines that The market now hosts a larger range of stable -coated that during previous cycles. Paypal launched Pyusd, World Liberty introduced USD1, Ethena launched Usde and Sky presented USDS.

Other names also emerge, including USDY from Ondo, USDG from Paxos and Ausd from Agora. These new projects are starting to attract investors and expand the overall base of the offer.

Compared to the previous cycles of the market, he notes that “There are many more credible stables than there were during the last wave, and they collectively have more offer than they had at the previous bullish market – even if Tether and Circle continue to dominate the market share and liquidity. »»

What distinguishes a lot from newcomers is their ability to redistribute the performance to holders. On the other hand, Tether does not provide any return, while Circle only offers limited rewards via partners like Coinbase. This makes the new stablecoins more attractive for holders in search of performance.

While the Genius Act frame formally restricts Stablecoins emitters from directly paying yields, it does not prevent third -party or intermediate platforms from offering rewards, often through agreeers with transmitters. According to him, this regulatory gap allowed models generating a yield to develop, giving new entrants an advantage over established players.

Genius does not really prohibit third -party platforms or intermediaries from paying rewards to stable -coxin holders (who are in turn paid to intermediaries by transmitters).

Nic Carter

Competition between Stablecoins should increase with the participation of banks

The recent regulatory changes also reconfigure the Stablecoins market by allowing banks and other financial institutions to issue their own documents. Carter notes that, although the concerns about possible banking parts persist, large banks actively explore their entry into this area.

Earlier this year, JPMorgan, Bank of America, Citigroup and Wells Fargo have held preliminary discussions on the formation of a stablecoin consortium. He explained that “A consortium has the most meaning, because no individually bank has the capacity to create the necessary distribution for a stablecoin that can compete with Tether. »»

The potential participation of banks could considerably expand the market. Carter explains that their entry could overshadow the current $ 300 billion market and create a new layer of competition for existing stablecoins.

Maximize your Cointribne experience with our 'Read to Earn' program! For each article you read, earn points and access exclusive rewards. Sign up now and start accumulating advantages.