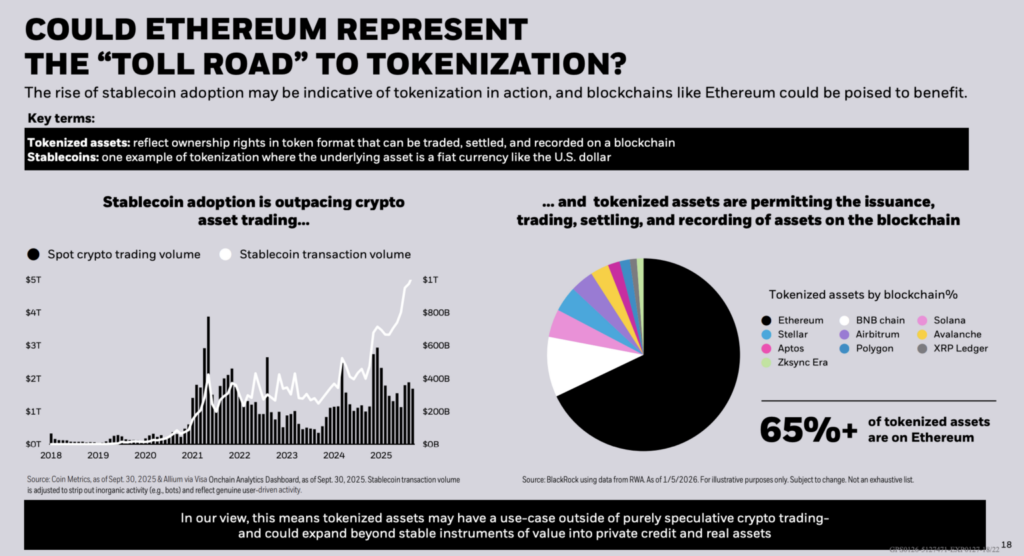

In its 2026 thematic outlook, BlackRock presents Ethereum not as a simple speculative asset, but as an essential financial infrastructure. The report describes the network as a potential “toll road” for tokenized assets, capable of capturing value through issuance, settlement and transaction fees as real-world assets are transferred onto it. For investors, the real question is whether growing tokenization activity will translate into sustainable economic demand for ETH.

In brief

- BlackRock positions Ethereum as a tokenization infrastructure, but avoids tying market share directly to the price of ETH.

- Rollups now secure most activity and value, weakening assumptions that tokenization growth is driving demand for ETH fees.

- Filtered stablecoin data shows that reported volumes overestimate actual usage, reshaping how investors evaluate the onchain economy.

- Multi-chain tokenization through BlackRock's BUIDL shifts the focus from dominance to settlement paths, fees, and demand.

Ethereum dominates share of tokenized assets, but BlackRock shifts focus to economic settlement

According to BlackRock, more than 65% of tokenized assets currently reside on Ethereum. This makes the network the leading base layer for tokenization today. However, the report refrains from directly linking this share to ETH price performance.

Instead, it focuses on the final location of settlement of economic activity and the networks that capture fees as tokenized liquidity and securities flow between blockchains.

Stablecoin data is crucial to this analysis. BlackRock notes that transaction volumes in its documents are adjusted to eliminate “inorganic activities,” such as automated transfers by bots. The company references data from Coin Metrics and Allium presented via Visa's Onchain Analytics dashboard.

This filtering method highlights a key limitation of raw onchain metrics: surface transfer volumes can significantly overestimate actual economic usage, particularly when investors attempt to infer throughput or fee generation.

Ethereum's current market share should be seen as a snapshot, not a permanent result. Data from the end of January shows significant variation depending on timing and methodology. The RWA.xyz directory lists Ethereum with a 59.84% share of tokenized real-world assetsrepresenting approximately $12.8 billion in value as of January 22.

Another view of the networks from the same platform also shows Ethereum leading by value, with around $13.43 billion excluding stablecoins, according to data timestamped around January 21.

The gap between these numbers and BlackRock's early January estimate highlights how quickly tokenization data can move. The show spans multiple channels, while reporting windows and asset classifications change from week to week.

Tokenization is progressing, but value capture by ETH remains uncertain in the era of rollups

For ETH holders, institutional adoption alone is not the deciding factor. What matters is whether the tokenization activity settles in a way that generates demand for ETH via fees or collateral.

BlackRock's thesis favors Ethereum as the base settlement layer for tokenized assets. This role, however, becomes more complex as execution moves further and further off the main chain. Rollups already secure large pools of value while handling most user activity.

According to L2BEAT, Arbitrum One secures approximately $17.52 billionand Base approximately 12.94 billion. Furthermore, OP Mainnet holds approximately 2.33 billion, with all three classified as stage 1 rollups.

This rollup-centric structure complicates the “toll road” analogy in several ways:

- Ethereum can remain the final settlement and security layer even if users rarely transact on L1.

- The assets used to pay fees vary between rollups, which affects how much value returns to ETH.

- Execution costs increasingly pile up on L2, displacing the appearance of daily activity.

- Security is inherited from Ethereum, but revenue capture is not guaranteed.

- Growth in rollup TVL does not automatically translate into increased L1 fee revenue.

Tokenized liquidity is a potential driver of future trading volume. Citi stablecoin report projects issuance reaching $1.9 trillion by 2030 in a base scenario and 4.0 trillion in an upward scenario. Assuming 50x velocity, Citi estimates annual transaction activity between $100 trillion and $200 trillion. At this scale, even small changes in the share of settlement between networks could have significant economic implications.

BlackRock and Visa cast doubt on raw stablecoin transfer metrics

As volumes grow, measurement becomes increasingly important. Visa argued that stablecoin transfer data contains substantial “noise.”

For example, Visa found that the reported monthly transfer volume of stablecoins had gone from 3.9 trillion to 817.5 billion dollars after exclusion of inorganic activities. BlackRock's support for similar filtering methods reinforces its focus on economically meaningful use rather than raw flow metrics.

If the “toll road” model depends on settlement, then organic demand that cannot be easily replicated elsewhere becomes the key variable. The multi-chain design weakens any simple link between tokenization growth and ETH demand.

Multi-chain tokenization redefines Ethereum's role as a settlement layer

BlackRock's tokenized fund, BUIDL, already operates on seven blockchains, with cross-chain interoperability provided by Wormhole. This architecture allows other chains to function as distribution and execution layers, even if Ethereum maintains a lead in settlement credibility or issuance value.

Several dynamics now influence how investors interpret tokenization data:

- The distribution of the issuance of assets across several L1s and rollups.

- Stablecoin metrics increasingly adjusted to exclude bot activity.

- Rollups change where fees are paid versus where security resides.

- Institutional products reduce dependence on a single platform.

- The location of settlement becomes more important than the gross transaction volume.

Questions have also emerged about whether institutional tokenization will converge onto a single ledger. During Davos week, this idea circulated online following comments attributed to BlackRock CEO Larry Fink. However, World Economic Forum documents released this month emphasize the benefits of tokenization such as fractional ownership and faster settlement without endorsing the idea that all assets will ultimately be settled on a single blockchain.

Ethereum's unresolved question is whether neutrality and decentralization can be maintained as regulated tokenization grows. Demands for transparency depend on the resistance to unilateral changes and the finality of the regulation on which the downstream layers rely.

Current data shows an expansion of rollups under the Ethereum security umbrella. At the same time, BUIDL's multi-chain deployment suggests that large issuers are actively protecting themselves against reliance on a single platform.

BlackRock's presentation on the “toll road” established a clear market share benchmark above 65% earlier this year. However, in late January, RWA dashboards and new product launches suggested that the near-term debate is less about dominance. Rather, it is about settlement paths, fee capture, and how organic usage is measured across the ecosystem of tokenized assets.

Maximize your Tremplin.io experience with our 'Read to Earn' program! For every article you read, earn points and access exclusive rewards. Sign up now and start earning benefits.