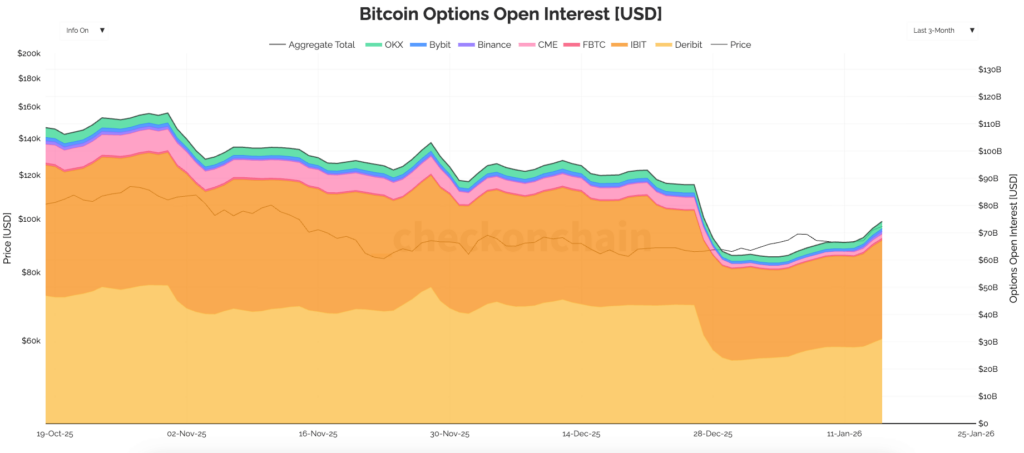

Bitcoin options open interest has surpassed that of futures for the first time, marking a turning point in how risk is spread across crypto markets. As of mid-January, options open interest reached about $74.1 billion, surpassing the roughly $65.22 billion recorded in futures contracts. This development reflects a market that relies less on short-term directional trades and more on structured positions, designed to manage risk and volatility over time.

In brief

- Open interest in Bitcoin options rose to $74.1 billion, surpassing that in futures and signaling a move away from short-term leveraged strategies.

- Options positions stay open longer due to time-based structures, shaping volatility around key strike levels and calendar rollover periods.

- The growth of ETF-linked options has fragmented bitcoin's volatility between U.S. market hours and continuously operating native crypto platforms.

- Futures continue to drive directional risk, but options now play a central role in how volatility and hedging flows influence price.

Bitcoin Options Sees Strong Rebuild After End-of-Year Expiry Cycle

Open interest measures the number of outstanding contracts still open, not daily trading volume. When the inventory of options exceeds that of futures contracts, positions tend to favor defined payoff structures, such as hedging or yield strategies, rather than simple directional bets on price. This change alters the price reaction around expiries, major strike levels and periods of reduced liquidity.

Futures contracts remain the most direct tool for gaining exposure to the direction of the bitcoin price. Traders post margin and incur funding costs that fluctuate with market conditions. Positions can be adjusted quickly, but they also react strongly to changes in funding rates or basis spreads.

Call and put options allow participants to limit losses, define upside potential or position themselves on volatility rather than the price itself. More complex structures, such as spreads or collars, often remain on the balance sheet for longer, because they are part of hedging mandates or planned return programs.

Options positions frequently remain open until maturity, making open interest structurally more stable. Conversely, futures positions fluctuate more, with traders adjusting their exposure based on funding pressures or exiting during de-risking phases.

Checkonchain data shows a clear pattern around the transition to the new year. The open interest of options fell sharply at the end of Decemberbefore rebuilding in early January, as new contracts replaced those that had expired. Futures open interest followed a steadier trajectory, reflecting continued adjustments rather than a sharp cleansing of positions.

Options Open Interest Becomes Key Signal for Hedging Flows

Options are often integrated into longer-term strategies, structured around rolling schedules. This makes inventory more persistent, even when price action seems hesitant or erratic.

- Futures positions incur ongoing carry costs through funding or basis variations.

- Options positions lock in a payment profile until maturity.

- Many options transactions are part of hedging or yield programs.

- Positions are often renewed according to fixed schedules, rather than readjusted in reaction to current events.

- Expiration mechanisms eliminate risk in blocks, not continuously.

Because of these characteristics, options open interest can remain high even as futures traders reduce their exposure. This persistence also influences volatility around expiration dates, particularly when large positions are concentrated at certain strike levels.

As the inventory of options increases, market makers play a greater role in shaping short-term price movements. Dealers who sell options typically hedge their exposure through the spot market or futures contracts. Depending on the distribution of positions, these hedges can either attenuate price movements or, on the contrary, amplify them.

When significant strike levels are close to the market price, hedging flows can intensify significantly as expiration approaches. Limited liquidity over certain time slots can amplify these effects, while deeper liquidity helps absorb them. Options open interest thus acts as a map indicating areas where hedging pressure is likely to increase.

Bitcoin Options Split Changes Trading Rhythms According to Market Hours

Bitcoin options are no longer confined to a single ecosystem. Alongside native crypto platforms, options linked to listed ETFs are gaining increasing importance. Data from Checkonchain shows increased activity around products such as IBIT.

Native crypto platforms operate 24 hours a day and use collateral denominated in digital assets. Their participants include proprietary trading firms, crypto funds, and experienced retail traders. Listed ETF options, on the other hand, are traded during US business hours and pass through systems familiar to equity options desks.

This segmentation modifies trading rhythms. A growing share of volatility risk is now concentrated on regulated, onshore markets, closed at night and on weekends. Offshore platforms, however, continue to dominate price discovery outside of U.S. hours, particularly during global macroeconomic events.

Ultimately, this separation could make bitcoin trading resemble that of stocks during American sessions, while retaining typically crypto behavior during off-peak hours. Traders active in these two segments often use futures contracts as a gateway, adjusting their hedges based on changes in liquidity.

ETF Options Shift Bitcoin Toward Portfolio-Like Risk Management

Compensation rules and margin requirements also influence the profiles of the actors authorized to intervene. Listed ETF options integrate with systems used by many institutions, opening access to companies that cannot operate on offshore platforms.

These institutional actors bring with them proven strategies. Covered calls, collar overlays and volatility targeting programs now appear via ETF options and repeat on set schedules. This regularity helps keep positions open and interest high, even when speculative demand declines.

Native crypto platforms continue to dominate continuous trading and specialized volatility strategies. What is changing is the nature of the motivations behind options positions, with an increasing share linked to portfolio overlays rather than short-term speculation.

When options outperform futures, market stress is expressed differently. Funding spikes and liquidation cascades become less important, while expiration cycles and strike concentration become key factors.

- Expiration dates can influence price trajectories more strongly than a one-time event.

- The concentration of strikes can draw support or resistance levels in the short term.

- Dealer covers can cushion or accentuate movements.

- Inventory reconstructions generally follow major deadlines.

- Futures remain a central indicator of directional risk appetite.

Monitoring options open interest by platform helps distinguish offshore volatility trades from onshore ETF-related programs. Futures open interest remains relevant in assessing the level of directional risk that traders are willing to bear.

Options open interest near $74.1 billion, compared to around $65.22 billion for futures, sends a clear signal: a growing portion of Bitcoin risk now resides in defined outcome instruments, structured around scheduled rollover mechanisms. Futures contracts, however, remain the primary tool for expressing a directional view and for hedging exposure generated by options.

Maximize your Tremplin.io experience with our 'Read to Earn' program! For every article you read, earn points and access exclusive rewards. Sign up now and start earning benefits.