For several quarters, we have witnessed an unprecedented decline in property prices since the great crisis of 2009. But is this a worrying signal? The rise in the interest rate, which largely explains this fall in prices, cuts off demand on the market. However, the fall in prices in the United States and the euro zone is still hesitant. A more marked decline in real estate prices would surely herald a future decline in the economy.

Real estate prices are falling

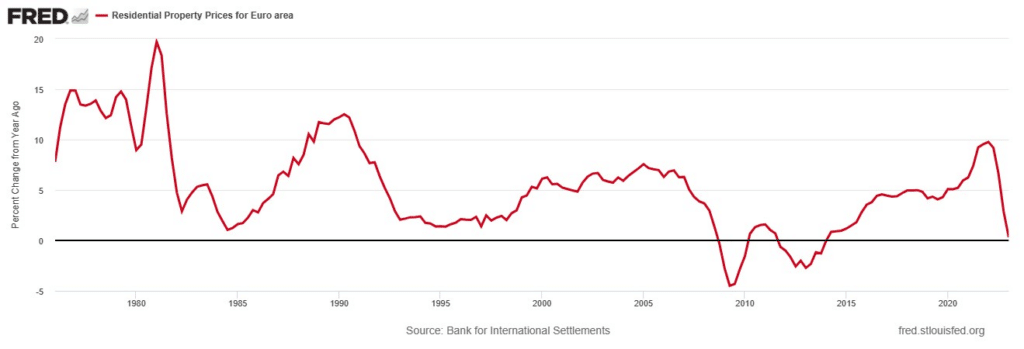

Between the third quarter of 2022 and the first quarter of 2023, the price of residential property in the euro zone fell by almost 2.7%. This drop must be analyzed in detail, because it may be a real bearish reversal. Over one year, property prices are stable in the euro zone.

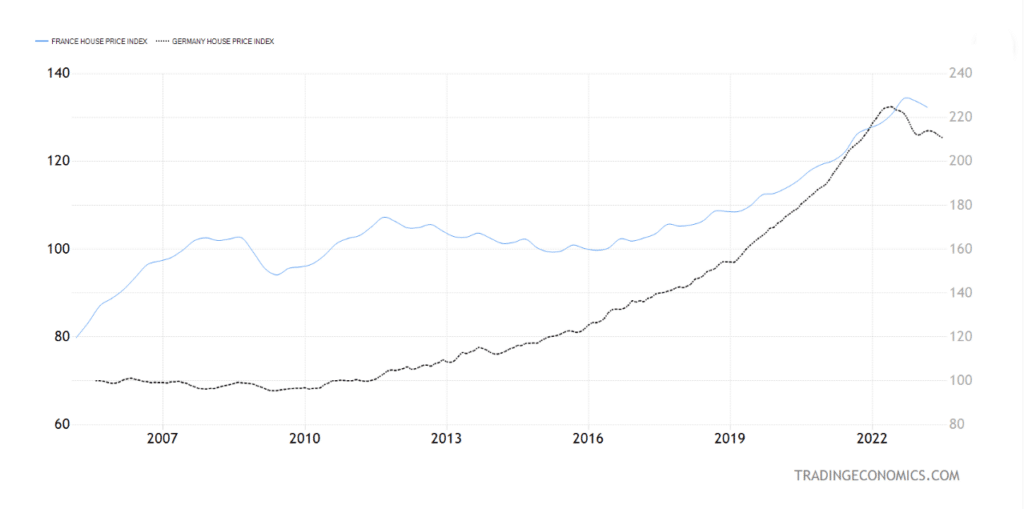

Despite everything, the cessation of the rise in real estate prices is well documented. In Germany, the latter began at the beginning of 2022. On the French side, the decline in real estate prices is less clear but just as effective. In the first half of 2023, sales would have decreased by 23% In France. In this lateral dynamic, large cities sometimes suffer the greatest declines. Over a year, the price of real estate in Lyon or Bordeaux would have fallen by 7% to 8%. But in Toulouse (+6%), Marseille (+2.5%) and Nice (+2%), property prices are expected to continue to rise. In any case, this shows that the fall in property prices, although structural, differs greatly from one country to another, and from one city to another.

An excessive rise in property prices

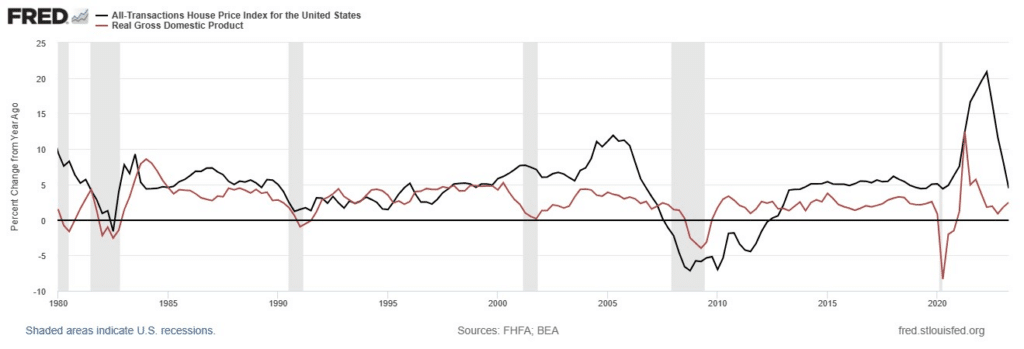

In general, real estate is a leading indicator of the economy. According to the adage, “when real estate goes, everything goes”. Indeed, we notice a sufficient correlation between the variation in GDP (of all income) and the variation in real estate prices. In a stable economy, where the demand for housing responds to the growth of the economy, the growth rate of real estate prices must be close to the increase in agents’ income. Therefore, the purchasing power conferred by real estate is constant and it allows the successful realization of economic needs.

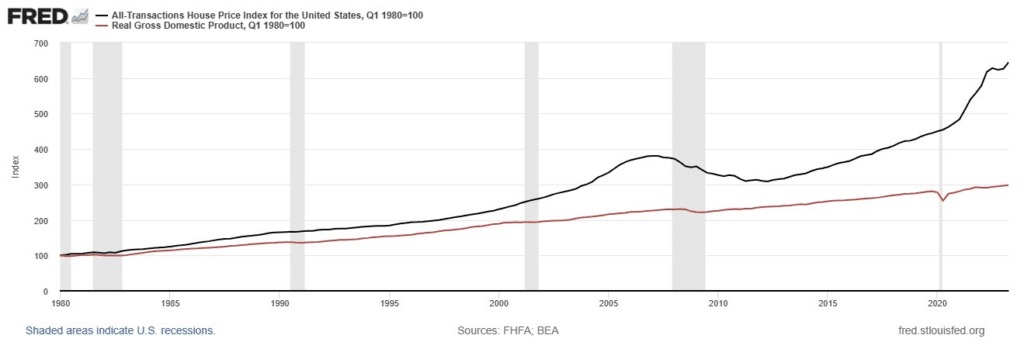

But in reality, real estate experiences phases of excess and depression. If the relative price of real estate has generally increased throughout economic history, this phenomenon has been particularly excessive in recent years. Since 2013, the growth rate of real estate prices has exceeded the growth rate of the economy in the United States. That is to say, to buy real estate you need proportionally more income than was required in the past.

Phases of excess or depression in the real estate market are often linked to the interest rate. When the interest rate is significantly lower than inflation or growth, households have every incentive to borrow. In this case, it is not uncommon to see real estate prices rise faster than the growth rate of the economy (this was the case from 2000/2002). Conversely, we witness a depression in the real estate market when the interest rate rises sustainably above the rate of inflation or growth of the economy.

A still hesitant decline

Consequently, if the key rate in the United States remains higher than inflation and growth, fundamental analysis suggests a decline in the real estate market in the long term. But the signals are slow to come…

It is remarkable that since 1980, the price of goods in the United States has increased by more than 50% in relation to income received. For the younger generations, it is therefore much more complicated to obtain a good at a reasonable price. In this sense, the fall in market prices appears as “desirable” long-term. This upward trend, which was slowed by the market crisis between 2007 and 2010, is now continuing. Despite everything, this study allows us to establish very relevant conclusions for the future.

Indeed, the price of real estate in the United States experienced a slight decline between the end of 2022 and the beginning of 2023. But the price increase continued between April 2023 and June 2023. The downward turnaround is therefore not yet really perceptible in the United States, where rate increases are nevertheless more significant. In general, the same dynamic could be observed in the eurozone in the coming months. This phenomenon can be explained by the fact that the growth rate of real estate prices has become sufficiently close to the growth rate of income, but the growth of real estate prices still remains higher…

New home sales remain stable

Likewise, most new home sales figures came in above expectations. We can clearly see that the confinements have marked a clear excess on the real estate market. This excess in 2020/2021 seems to have been offset by a symmetrical trough. This dip in the real estate market appears to have been accompanied by a slight drop in prices. Sales of new homes are now holding up, but the upward trend observed since 2011 is clearly affected.

The rise in rates in question

Two phenomena explain the stagnation of the real estate market so far. On the one hand, this is a correction phenomenon in the face of the excesses observed in 2020 and 2021. On the other hand, the return of inflation has pushed banks to drastically increase the borrowing rate.

“ On the one hand, the ECB was slow to raise its rates. Indeed, the ECB began to raise its rates from September/October 2022, compared to March 2022 for the FED. An increase in rates until the end of 2023 at least for the ECB would therefore not be incongruous or difficult.

On the other hand, inflation in the euro zone is more persistent and more structural than in the United States. Which would justify an increase in the key rate at least to the level of the FED key rate. The latter is currently at more than 5%. Under these conditions, we understand that the ECB, usually more attentive to budgetary issues, is encouraged to pursue a more aggressive strategy.“

The rise in rates hardens in the euro zone – Tremplin.io

The cost of credit is therefore clearly increasing, and the increase from a rate of 1% to 3% is enough to increase monthly payments by almost 20%… Some households must therefore abandon their project or lower their requirements.

Are other markets holding up?

The decline in house prices is often correlated with most other assets. After a pitiful 2022, 2023 marks a slight rebound on the stock markets. Furthermore, the price of cryptocurrencies has recovered since the start of 2023. But here again, we are seeing stagnation rather than a real decline. This phenomenon is characteristic of periods of inflation.

Therefore, the risk of recession is probably the main risk to take into consideration. Indeed, even if wages increase with low unemployment (and therefore borrowing capacities), and the results of companies manage to progress, a recession would bring a significant halt to the investment capacities of households and businesses. For now, the recessive signs show us a risk within 18 months to 36 months. However, weakness in the economy can become apparent quickly.

In this context, any drop in real estate, stock market indices, or markets in general, should be interpreted as a powerful warning.

In conclusion

Ultimately, the real estate market suffers a decline due to two effects. The first effect is that of a correction which follows the excesses of the market in 2020/2021. The second effect is more obviously the increase in rates, which considerably reduces the borrowing capacities of agents. But the decline in property prices differs from city to city, from country to country. In the eurozone, the decline in prices is very real, as well as in the United States. However, we note that this drop in prices has stopped in recent months, and this is reflected in the sales figures.

In some cities, on the contrary, the drop in prices is very real and quite significant. If it is clear that the rise in rates is expected to continue over the next 6 months, the challenge will be to observe the resilience or weakness of the real estate market. Finally, it is remarkable that the main risk weighing on most assets remains the risk of recession. The recession, in addition to rising rates, could cause a more lasting turnaround in the real estate market.

Receive a summary of the news in the world of cryptocurrencies by subscribing to our new service daily and weekly so you don’t miss anything of the Tremplin.io essentials!